How to Buy Crypto With a Bank Transfer

If you’ve ever sent a bank transfer and then refreshed your balance every few minutes waiting for it to arrive, you’re not the only one.

The process sounds simple: send money from your bank account, wait for the balance to update, and start using it. But in practice, transfers don’t always move as quickly, or as cleanly, as people expect.

Sometimes the funds arrive within hours. Sometimes they take longer. Occasionally, the final amount is slightly lower than what was sent. That’s usually when the back-and-forth begins: checking the app, checking the bank, then checking the app again trying to figure out where things are stuck.

Most of the time, nothing is actually wrong.

Funding a crypto balance from a bank account still depends on traditional banking infrastructure. Cutoff times, processing windows, weekends, holidays, and intermediary banks all affect how quickly a transfer moves and how much ultimately arrives.

Once you understand that, the process feels a lot less unpredictable.

This guide explains how bank transfers work when funding a crypto balance, why delays happen, where fees usually come from, and what to check before assuming there’s a problem.

How Funding by Bank Transfer Works

When you fund your balance through a bank transfer, the process is fairly straightforward. First, you get the deposit details inside the app. Then you send a transfer from your bank using those details. After that, the transfer moves through the banking system until it’s processed and credited on the receiving side.

The important thing to remember is that banks process transfers in batches and windows - not continuously in real time. That waiting period is what causes most of the confusion. Even if your bank shows the transfer as “sent,” the receiving side may still be processing it.

Once the transfer clears, the balance updates automatically and becomes available for spending.

Why Transfers Sometimes Take Longer Than Expected

One of the most common misunderstandings is assuming that “sent” means “received.”

When your bank confirms a transfer, it usually means the funds left your account. It does not necessarily mean the receiving bank has processed and credited the transfer yet. Timing matters more than most people realize.

If you send a transfer late in the day, outside business hours, or before a weekend or holiday, the payment may wait for the next processing window before moving forward.

First-time transfers can also take longer. Banks often apply additional checks when:

- You’re sending to a new beneficiary

- Using a new payment route

- Or transferring a larger amount than usual

After the first successful transfer, future payments on the same route often move faster.

Why the Final Amount Can Be Lower

If the amount received is slightly lower than the amount sent, intermediary banking fees are usually the reason. International transfers in particular can involve several parties:

- The sending bank

- Intermediary banks

- The receiving bank

- And local payment systems

Any of them may apply fees during processing. In most cases, the receiving platform is not adjusting the amount after arrival - the deductions usually happen somewhere within the banking route itself.

That’s why the final credited amount can differ slightly from what originally left your account.

Choosing Between Bank Transfers and Stablecoins

Even if the app presents everything through a single “deposit” flow, different payment rails behave very differently underneath. Bank transfers tend to be slower, but they’re familiar and relatively predictable once you understand how processing windows work.

Stablecoin transfers are often much faster, but they’re also less forgiving. Network selection, wallet addresses, and transfer details must all be correct. A small mistake can send funds to the wrong destination or delay recovery. For many people moving money from a traditional bank account into crypto for the first time, bank transfers feel simpler because the process is already familiar.

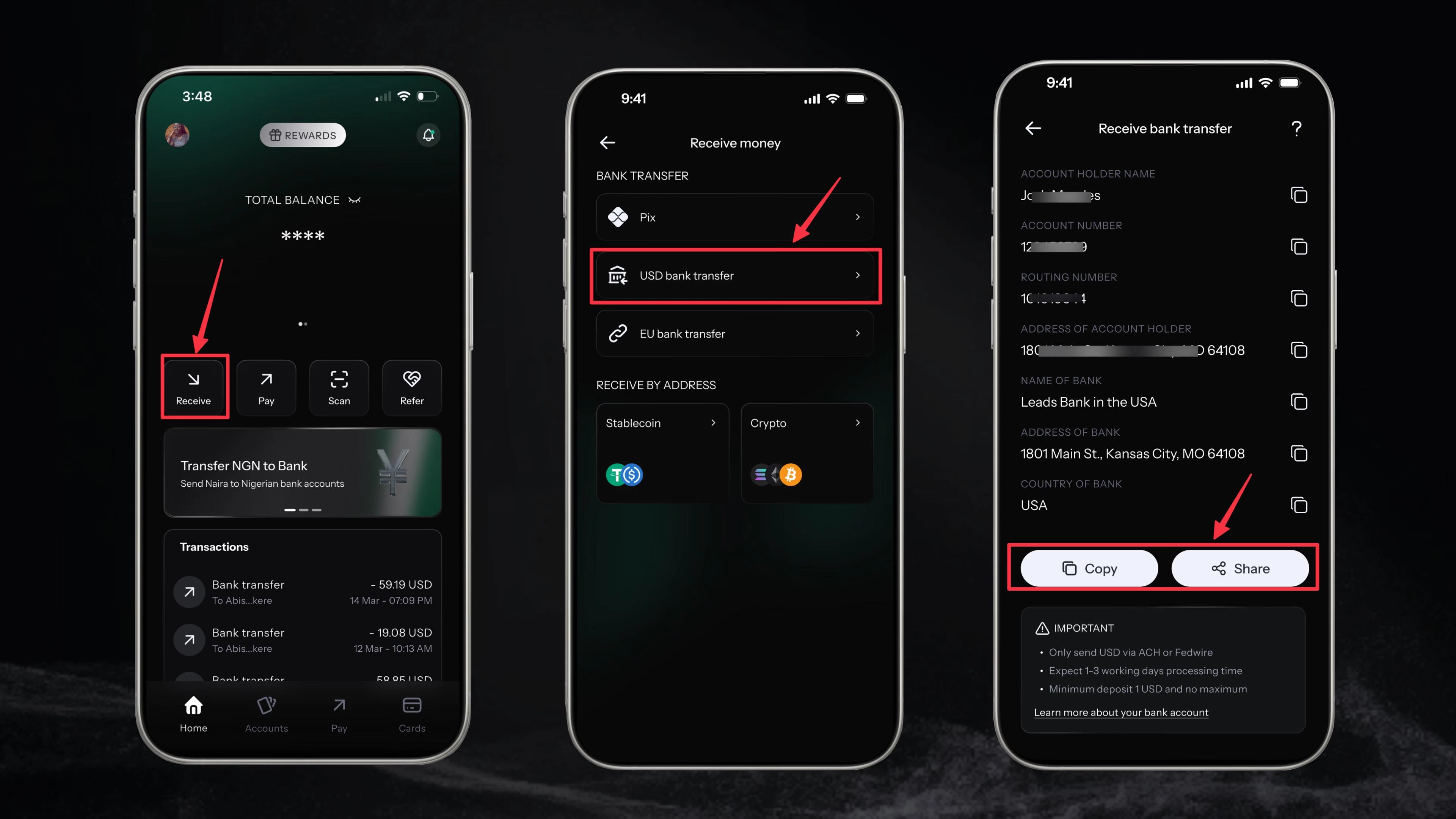

How to Move Money From Your Bank Account Into KAST

The process itself is simple:

- Open the app and go to Add Funds / Deposit → Bank Transfer

- Choose the transfer rail available to you (such as ACH, SEPA, SWIFT, or a local transfer method)

- Copy the deposit details exactly as shown

- Initiate the transfer from your bank account

- Wait for the transfer to complete its processing window

The transfer method you choose affects both timing and possible intermediary fees

If the transfer takes longer than expected, the most common reasons are:

- Bank cutoff times

- Weekends or holidays

- First-time beneficiary reviews

- Or intermediary banks in the transfer route

Where Transfer Fees Usually Come From

Bank-funded crypto deposits often involve multiple layers of fees rather than one single charge. Depending on the route, fees may come from:

- Your bank

- Intermediary banks

- The receiving bank

- Or local payment systems

That’s especially common with international transfers.

On the platform side, deposit fees can also vary depending on the transfer rail. For example: KAST charges $2 for an ASH deposit and $15 for a FedWire deposit. As for local

deposits, ARS and SPEI transfers have a 0% fee, while PIX transfers have a 1% fee.

If the final amount is slightly lower than expected, fees somewhere along the banking route are usually the explanation.

Quick Checks Before Troubleshooting

Before assuming a transfer failed, it’s worth checking a few basics.

Make sure:

- The deposit details were copied exactly

- The correct transfer rail was used

- The transfer wasn’t sent outside processing hours

- And the bank confirmation doesn’t mention intermediary fees

If it’s your first time sending to that destination, additional review time is also fairly common.

Most transfer issues come down to timing or banking fees rather than an actual processing failure.

Moving Stablecoins Back Into a Bank Account

The reverse process works a little differently.

Banks do not receive stablecoins directly. Before funds reach a bank account, the stablecoins are first converted into fiat currency, then sent through standard banking rails like SWIFT, SEPA, ACH, or local networks.

Once you separate the crypto side from the banking side, the flow becomes much easier to understand.

Spending With a Crypto-Funded Card

When using a crypto-funded card, the setup behind the scenes may involve stablecoins, but the payment itself still runs through traditional card networks.

The merchant receives fiat currency just like any standard card transaction.

If a payment appears as “pending,” that usually reflects the normal gap between authorization and settlement - a standard part of how card payments work.

What to Keep in Mind Before You Send

If you’re moving money from a bank account into crypto, it helps to think about the process as a normal bank transfer first.

That means:

- Timing matters

- Transfers move in processing windows

- And fees can appear at multiple points along the route

Once you understand those basics, the process feels much more predictable.

You know roughly when the transfer should arrive, why delays happen, and why the final amount may not always match exactly what was sent. Most importantly, you spend less time guessing what’s happening in the background.

Explore KAST here